1. Introduction

The importance of Entrepreneurship has increased thanks to the astonishing performance of Innovative start-ups and their positive impact on the economy. In the case of Korea, by hiring 66 thousand people in 2021, the Ministry of Small Medium Enterprises and Start-ups (MSME) (2022) indicates that the innovative Korean venture and start-ups tracts the Korean economy significantly. Also, as Korea's Small Medium Enterprises take charge of 99.9% of total companies and hire 82.7% of the entire labor force, SMEs are considered the stem of the national economy. Furthermore, by generating 2,732 trillion Korean won, the economic impact of SMEs cannot be ignored (MSME, 2021).

Thus, after industrialization, governments have struggled to create a business-friendly ecosystem to stimulate business. However, after the discussion about the destructive entrepreneurship, which lead to the innovation of the company, rose from the Schumpeter, Entrepreneurial Ecosystem (EE) has been highlighted as a macro-environment that not only maintain and operate the business but influence business operation quality and performance by evoking innovation (Moon & Chang, 2015). Therefore, there are various meaningful efforts to identify EE and measure entrepreneurship. Global Entrepreneurship Monitor (GEM) conducts measurement of entrepreneurship in the countries, and the Global Entrepreneurship and Development Institute(GEDI) evaluates the EE through Global Entrepreneurship Index(GEI) based on the entrepreneurship aspiration, abilities, and attitudes (GEDI, 2019; GEM, 2022). However, as EE can interact with the nation’s economy, business, culture, society, technology, and so on, there is a need to analyze the relationship between the macro-environment of the nation and its EE based on the potential performance targets.

For instance, as a subject of the national economy, various countries support and encourage innovative entrepreneurs to foster competitive SMEs. However, despite various supports and aid suggested and implemented by each government, the validity of policies is suspicious whether the policy successfully results in performance improvement and entrepreneurship encouragement of the SMEs. In addition to the doubt, in recent days, there has been a demand for adjusting the current supporting policy focusing on succoring marginal businesses from the suffering of the over-competitiveness, economic depression, and management crisis caused by global pandemic issues into building a competitive entrepreneurship ecosystem that can encourage innovative ideas (Jung, Lee, & Yun, 2021).

Thus, this study agrees with these policy demands and aims to verify the significant components contributing to EE to enhance the EE policy quality. Compared to the studies conducted with survey data for comparing different EE by nations, this paper has differentiation and scarcity, which are distinct from other studies by using the time-series data to construct predictive models and economic data for quantitative relation analysis with the Multiple Linear Regression (MLR). For the research direction of this paper, firstly, it aims to identify the components of the EE from the perspective of quantitative macro-environmental data and select the PESTEL model as a framework to categorize the data variables. Assume that superior EE can contribute to the emergence of a unicorn company, its economic value, new business creation, number of enterprises, employment increase, involvement of employers and employees, and entrepreneurship, this study conducts a MLR model analysis to examine which factors are important in EE and can maximize the performance. Through this study, this paper expects to develop an EE framework that can predict the tentative performance using the machine learning method. Through the result, this paper seeks to identify the components of EE in terms of quantitative macro-environmental data and verify the usefulness of the PESTEL model as a framework for classifying data variables.

2. Conceptual Background & Literature Review

2.1 Entrepreneurship

Say, the French Economist, defines entrepreneurship as shifting economic resources for higher productivity around 1800 (Drucker, 2012). However, Schumpeter expands the entrepreneurship concept, which transmutes the internal resource, ideas, and invents as successful innovation (Mehmood et al., 2019). Schumpeter also insists on the role of entrepreneurs who evoke creative destruction, destroying the traditional method and changing the market structure with innovative ideas. Thus, entrepreneurship is the major motivation of innovative SMEs, which lets them challenge the existing market by bringing innovative ideas. Due to the cohesive relationship with SMEs, entrepreneurship can be confused with a startup. However, though the startup process can be a part of entrepreneurship, entrepreneurship is not limited to the startup process but the overall business life cycle. Thus, Gartner (1985) considers entrepreneurship as a process dynamic among the individual, organization, and the environment. As Gartner’s argument, there are various components cultivating entrepreneurship, Driessen and Zwart’s (2002) approach from internal and external aspects such as characteristics of the entrepreneurs and organizational- and market environments.

In Driessen and Zwart’s contention, entrepreneurship can be defined as internal components of entrepreneurs such as characteristics, entrepreneurial style, and managerial competencies (2002). Likewise, entrepreneurship can be determined by those entrepreneur’s characteristics: motivation, risk, leadership, knowledge, innovativeness, and so on, however, these should correspond with internal organizational factors like goals, strategies, and external factors such as organizational and environmental factors. This can be also observed from the case of global innovative countries like Amazon and Apple, which succeed with solid entrepreneurial leadership, however, the environmental factors also cannot be ignored since, according to the CB insights (2022), compared to the United States and China which attains 585 and 174 unicorn companies, except 11 countries which have more than ten unicorn companies, 35 countries have unicorn companies less than 10. This regional bias in the distribution of the Unicorn company implies that there is a superior entrepreneurial ecosystem making outstanding performance.

Thus, there are various attempts to measure and evaluate entrepreneurship as the key to success. Corporate Entrepreneurship Assessment Instrument (CEAI) is one of the methods which measure the internal organizational factor of the company, which influences the business activity and performance. Under the CEAI, there are top management support, work discretion, rewards and reinforcement, and time availability (Holt, 2015). Since it indicates whether the entrepreneurs encourage its organization to develop innovativeness and challenge, it is significant to review whether the company has innovativeness competence. In a similar context, as the importance of the business environment influencing the business has been highlighted, the study on the entrepreneurial ecosystem is also proactively conducted.

2.2 Entrepreneurial Ecosystem

The “Entrepreneurial Ecosystem (EE)” is generally defined as the interactive business ecosystem that mainly supports the rise of ventures (Liguori, Bendickson, Solomon, & McDowell, 2019). Though "Business Ecosystem" has been used frequently in the study of Moore (1993) as the term describing the holistic ecosystem influencing overall operation and management of business under business cycle, the concept of Entrepreneurial Ecosystem, which is also called "Start-up Ecosystem," becomes specified as a framework by Isenberg in 2010. Entrepreneurial Ecosystem Framework explains how policy, market, finance, culture, support, human capital, etc., stimulate innovative entrepreneurs' emergence (Isenberg, 2011). The Isenberg model, as in Table 1, describes the sub-elements of the entrepreneurship ecosystem from the perspective of Government, Financial Capital, Leadership, and others that formulate the pro-business environment and enhance the creativity of entrepreneurs (Isenberg, 2011).

After the study of the Isenberg, the interest in the entrepreneurship ecosystem has increased continuously, though according to the Dimensions (2022), after it peaks at 18,862 publications in 2020, it has dropped significantly, as shown in Figure 1. However, the study on the entrepreneurial ecosystem has been actively conducted worldwide, especially in China, the United States, and European Countries. Therefore, under the situation of the global pandemic, the study about the impact of global crises such as Covid-19 on the entrepreneurship ecosystem was also proactively studied. As it analyzed in Figure 1, using word association analysis denoted on word clouding, those studies about the various frameworks and EE imply that innovative companies not only depend on individual features of entrepreneurs but also can be cultivated by macro-environmental factors such as education, innovation, public, policy, and others.

In one of the previous studies, Davari and Najmabadi (2018) conclude that support, finance, culture, policy, market, and others have a high influence on the perceived entrepreneurial performance among eight EE components that influence entrepreneurial performance when using the simple linear regression method. However, this paper also conducts the MLR model analysis and concludes that support, finance, infrastructure, and policy have significant relation with EE. Though this study is limited to the Iranian case and the data is collected by survey, it proposes significant insights to business and policymakers about the cause and effect of EE.

Beyond the scholarly study, Global Entrepreneurship Monitor(GEM) and Global Entrepreneurship and Development Institute(GEDI) analyze the global EE. GEDI releases the annual Global Entrepreneurship Index(GEI) based on the entrepreneurs' aspirations, abilities, and attitudes within institutional and individual variables reflecting the compiled data of the economic activity (GEDI, 2019). GEM's comparison of entrepreneurship among countries through the Entrepreneurial Ecosystem Quality Composite index (ESI) analyzes a sequence of the way that the social, cultural, political, and economic context of entrepreneurial and national conditions lead to entrepreneurial activity, entrepreneurial output as new jobs, new value-added, social-economic development outcomes and how it re-influence into environmental factor. Through National Expert Survey, GEM compares distinctive EE on Economic Framework Conditions (EFCs) like financing, market access, policy, R&D, and so on, with the general attitude, perception, motivation, and activity of national entrepreneurs (GEM, 2022). Furthermore, as indicated in the OECD's case study about the Policies for entrepreneurial ecosystems, various governments struggle to construct a competitive entrepreneurship ecosystem to cultivate innovative entrepreneurs and unicorn companies (Mason & Brown, 2014).

Thus, to build successful ventures, innovative entrepreneurs and entrepreneurship should be prerequisites. However, as it is difficult to control an individual's unique talents, government policy to cultivate innovative entrepreneurs would be systemic as EE. Though various previous studies define the entrepreneurial model as a venture company, venture capital, venture market, infrastructures, network, and other external factors as the Isenberg model, to analyze the entrepreneurship ecosystem quality on the alignment of the macro- business environment, this paper dissolves the entrepreneurial ecosystem elements and assigns those elements based on PESTEL model.

Considering the complexity of macro-environmental factors that can influence the quality of the Entrepreneurial Ecosystem, this paper defines an entrepreneurial ecosystem as a certain business ecosystem that focuses on cultivating innovativeness and the spirit of challenges. Assume that governmental entrepreneurship policy aims to produce fair ventures regardless of the input, such as the company's or entrepreneur’s features, if the government attains a fair quality of entrepreneurial ecosystem, the outcome such as GEI, high employment, high economic value creation by ventures, the emergence of a unicorn company, etc. should be generated. Therefore, assuming that the performance of entrepreneurship becomes maximized when there are proper entrepreneurship ecosystem factors matched with the business lifecycle, the model in Figure 2 presumes that an entrepreneurship ecosystem should consider overall macro factors from business development, start-up, growth, maturity, and exit so that it can support stable exit of business from market or transition to the other field or further expansion. Thus, though Brown and Mason (2017) indicate that the input from entrepreneurial actors and institutions returned to the output of value-added and competitive advantage depends on the entrepreneurial ecosystem, this paper considers EE as a macro-environment that stimulates and supports the innovation of entrepreneurs: Politics, Economics, Social, Technology, Environment, and Legal. However, though factors such as ESG (Environment, Social, Governance) can influence entrepreneurship, since there is no international official index to measure, this paper replaces the Environment factor with the Finance factor reflecting previous EE studies specifically as Isenberg model which allows entrepreneurs to secure the capital which also can be a sub-category of the Economic factor.

3. Methodology

3.1 Research Model

Based on the EE defined through literature review in the conceptual background, this paper collects data and constructs the EE quality model through the PESTEL framework. Whether PESTEL, the quality of the startup ecosystem, affects innovation, startup, employment, business activity, involvement, expectation, and GEI performance can be examined with the following model (Figure 3).

The collected data categorized into the PESTEL framework should be preprocessed to avoid multicollinearity and over-fit issues. Therefore, to identify the relationship between entrepreneurial performance and EE quality, this paper conducts an MLR analysis. Through the step wising MLR method, this paper selects significant factors that influence performance and determine the EE so that policymakers can judge the current EE and predict the potential performance by EE factors. Therefore, for the accuracy of the model, the Receiver Operating Characteristic curve (ROC) and Area under the ROC Curve (AUC) methods are used to determine models with high explanatory power based on the AUC value and R-squared value with the process in Figure 4.

3.2 Data Description

To analyze the EE, this paper collects data from world public organizations released by OECD, WB, CB Insights, and UNDP from 2000 to 2021. This paper collects data with 5830 observations with 109 variables from April 6, 2022, to April 12, 2022. Therefore, as the element of constructing entrepreneurship has been studied by Global Entrepreneurship Index (GEI) and Global Entrepreneurship Monitor (GEM), this paper also uses the open data from GEM and GEI as a socio-cultural factor. Therefore, this paper categorizes the dataset based on PESTEL components based on the assumption that components under the PESTEL framework determine the entrepreneurship ecosystem and uses the country code as an identifier (Table 2).

For the independent variables, the variables related to the direct government activity, such as governmental support, taxes, etc., are categorized into policy. As these variables from GEM are studied as scores that indicate the perception of the respondent, they are discrete from economic factors indicating monetary value released from the world bank. Thus it includes trade, national production, and fiscal expenditure on researchers which can have overlaps with technology and policy. The finance index denotes nations' accessibility to financial resources from investment to liability. Technology also implies not only the Research and Development (R&D) level but technological infrastructure which also can be social value bit sorted in technology considering the technological aspect more significantly. Therefore, in contrast to the policy, which includes overall governmental support and policies that influence entrepreneurship, regulation and legislation focus on the negative variables influencing doing a business and can determine entrepreneurship. Social factor indicates a broad range of social aspect from culture, education, the general perception of entrepreneurship, business attitude, social infrastructure, labor force, networking, and so on that are also mainly constructed with quantitative measurement from GEI and GEM (Table 3).

Excluding variables categorized under the PESTEL framework for independent variables, this paper sets the number and valuation of unicorn companies as a dependent variable to measure the innovative performance of the ecosystem since the unicorn company implies it has innovative and competitive business to achieve high market value. Also, since policymakers encourage entrepreneurship policy to enhance national economic growth and social stability, to measure whether the entrepreneurship ecosystem contributes to the nation's market growth, employment, and involvement of entrepreneurs, the number of new businesses, employment, entrepreneurial activity, and global entrepreneurship index are used as dependent variables for each model. However, GEI can be used as both outcomes of EE but also as a social factor in constructing EE, this should be a parameter variable. Yet, to explore the relationship between EE performance and GEI as an independent variable and EE quality and GEI as a dependent variable, this paper set hypotheses that have GEI as independent and has it as a dependent separately (Table 4). As indicated in Table 4, each relationship between EE components and performance variables would be tested through MLR models based on the hypotheses. For instance, assume that the EE has a significant influence on the unicorn value, this assumption will be hypothesis 1, and the MLR model to validify the hypothesis will be model 1. For the sake of simplicity, this paper denotes model 1 as M1 and hypothesis 1 as H1 and applies the same denotation to the other hypotheses and models.

3.3 Research Hypothesis

Models 1 and 2 developed from hypotheses 1 and 2 that have innovation as EE policies target. This paper considers the number of unicorn companies and their economic value as an innovation index since EE policy can contribute to increasing the quantity of unicorn companies and both increasing their quality by having high market value.

H1: The quality of the entrepreneurship ecosystem has a significant impact on the number of unicorn companies

H2: The quality of the entrepreneurship ecosystem has a significant impact on the value of unicorn companies

The third hypothesis aims to measure the encouragement effect of start-ups, and the fourth hypothesis tries to observe the employment effect of the entrepreneurial ecosystem. The fourth hypothesis is based on the argument of Vogel (2013), who insists that a fair entrepreneurship ecosystem can alter youth from job-seeker to job-creator. Also, the fifth hypothesis based on a superior entrepreneurship ecosystem has the effect of stimulating the nation's economy by generating and sustaining businesses. Thus, the fifth hypothesis sets the number of enterprises as a dependent variable for business activity, not only limited to start-up level businesses.

H3: The quality of the entrepreneurship ecosystem has a significant impact on the new business registered

H4: The quality of the entrepreneurship ecosystem has a significant impact on the employment

H5: The quality of the entrepreneurship ecosystem has a significant impact on the number of enterprises

The sixth and seventh hypotheses intend to measure the entrepreneurship of business owners and employees influenced by EE. Entrepreneurship of business owners and employees is measured through the survey from GEM named as employees' and business owners' involvement. Also, based on the assumption that EE can generate optimistic economic expectations and job expansion expectations (Autio, 2005), the eighth hypothesis would be tested with high job creation expectations studied by GEM. The eighth hypothesis presumes that a high entrepreneurship ecosystem contributes to public expectation for employment and results in social stability. Since the purpose of establishing an entrepreneurship ecosystem policy is based on enhancing economic competitiveness and social stability from economic growth, this can be a performance objective of a fair entrepreneurship ecosystem (Kelley, Singer & Herrington, 2012).

H6: The quality of the entrepreneurship ecosystem has a significant impact on the involvement of entrepreneurs in business activity

H7: The quality of the entrepreneurship ecosystem has a significant impact on the involvement of employees in business activity

H8: The quality of the entrepreneurship ecosystem has a significant impact on employment expansion

Though the hypotheses above assume that the entrepreneurship ecosystem contributes to quantitative economic performance and social stability, the ninth hypothesis analyzes whether the macro-environment factors forming the entrepreneurial ecosystem influence on entrepreneurship of the entrepreneurs. The GEI variable is performed as the dependent only for the ninth model and is performed as a social factor on the other models from one to eighth.

H9: The quality of the entrepreneurship ecosystem has a significant impact on the entrepreneurs’ entrepreneurship

3.4 Methodology

After these data collection and hypotheses setting, to manage the missing values, this paper imputes mean values and the hot-deck method to avoid the bias caused by missing values. Therefore, based on these hypotheses, this paper conducts Multiple Linear Regression (MLR) analysis to determine significant variables that determine EE. Using a supervised machine learning MLR analysis that allows predicting value with training, valid, and test data-set. Though Stam. E. (2018) develops the entrepreneurship ecosystem measurement method by using the multivariate linear regression model, this paper aims to identify the significant components of the entrepreneurial ecosystem influencing each entrepreneurship performance by using the stepwise MLR through the MASS package in R to simplify the model. However, before setting the stepwise MLR, a full multiple linear regression model as Formula 1 should be developed. Based on the full MLR model, by adding and subtracting variables in steps, the stepwise model with optimal R-square can be detected.

For each predicted MLR model as Formula 2.b., they have the independent variables to measure the performance of the EE as dependent variables denoted as y-hat such as the number of unicorn companies, their value, the new business registered, employment, number of enterprises, Ownership, Employee activity, Job creation expansion, and entrepreneurship index. Through Formula 1, the R-squared value can be calculated as Formula 2, which indicates the explanatory power of the linear regression model (Senthilnathan, 2019).

However, due to the amount of data, the R-squared values of nine models were excessively high, over 0.9. Though this high value of R-square value can indicate the high explanatory power of the model, this can also denote the multi-collinearity issue. To avoid multicollinearity issues that occurred when the independent variables have a correlation, this paper utilizes the Variance Inflation Factor(VIF). VIF is the estimating variance ratio of the multiple parameters with models with by parameters as on the step on the Formula 3.a. and through calculating R-square value through formula 1 and 2, VIF can be calculated as Formula 3.b. (Senthilnathan, 2019)

Therefore, for MLR analysis, the dataset should be split into training, test, and validation set. To reduce the uncertainty of the global pandemic issue, this paper mainly utilizes a 2018 dataset as a test set and uses the other dataset as training and validation sets to conduct the machine learning by 0.7 and 0.3 ratios. Constructing the MLR model with the training dataset, this paper verifies the performance with the validation dataset and conducts MLR analysis with the test dataset. In this paper, the MLR models with test datasets have been analyzed. On the MLR analysis, this paper considers that R-squared values over 0.8 are reasonable and determines significant components under the 95% confidence level so that the variables with a p-value below 0.05 are considered meaningful.

Furthermore, to verify the performance of the MLR model, this paper uses binary classification in the MLR model based on the logarithm transformation. Using the prediction of the MLR derived from the test dataset, transforming it into log values that can be categorized into True (1) and False (0). After conducting MLR analysis with training and validation datasets, this paper conducts logarithm transformation to build a confusion matrix with binary classification. when the predicted value is similar to the expected value, which is the dependent variable, this classification categorizes the value into True or else False. The confusion matrix is a method to measure the performance of a machine learning algorithm by comparing predicted and actual values as Figure 5 (Park & Kim, 2018). Based on the confusion matrix from binary classification, this paper evaluates the performance of models through ROC (Receiver operating characteristic) curve and AUC (Area Under the ROC Curve) (Park & Kim, 2018). The AUC-ROC curve which has the true positive rate on the y-axis and the false positive rate on the x-axis can be constructed as it is in Figure 5. Thus the area under the curve indicates the accuracy of the model. Since AUC over 0.7 is regarded as acceptable, over 0.8 is regarded as fair, and over 0.9 is regarded as excellent, this paper considers a model with AUC below 0.7 as an inferior model (Park & Kim, 2018).

4. Result

4.1 VIF Verification

To overcome over-fit and multicollinearity issues, this paper conducts VIF verification on the collected datasets using the constructed MLR model from developed hypotheses. Since from models 1 to 9, the variables with high VIF were the same, this paper dropped variables with VIF>10 since variables with VIF between under 5 to 10 are acceptable and have ignorable multicollinearity (Ha et al, 2021). As in Table 5 which is the example of full MLR model 1(M1), 56 variables have a correlation with each other.

Thus, this paper matches the variable which has high correlations with others and drops which has higher VIF and has dropped 20 variables that have overlaps with other variables. For instance, since Gross Domestic Production(GDP) overlaps with GDP growth, this paper drops GDP with a higher VIF. Then, after dropping GDP, and recalculating VIF after dropping GDP, among variables with high VIF, this paper drops the total population since this can be replaced by an economically active population(POP). Likewise, this VIF method has been done in steps until all VIF of variables is adjusted to below 10.

4.2 Multiple Linear Regression

Based on the hypotheses in the methodology, with the 79 variables excluding multicollinearity issues, the full MLR model as Formula 4. has been developed. Based on the hypotheses in the methodology, with the 78 variables excluding multicollinearity issues, the full MLR model as Formula 4. has been developed. Each model has the dependent variables to measure the performance of the entrepreneurial ecosystem such as the number of unicorn companies, their value, the new business registered, employment, number of enterprises, Ownership, Employee activity, Job creation expansion, and entrepreneurship index. Models using first to eighth hypotheses follow the formula 4, however, hypothesis 9 does not contain the GEI variable and coefficient β93.

(Formula. 4.)

Using the full models, and conducting a stepAIC algorithm in R, this paper simplifies the model remaining statistically significant variables. Based on the full multiple linear regression model in Appendix. 1, the stepwise MLR model can be concluded in Tables 6-7.

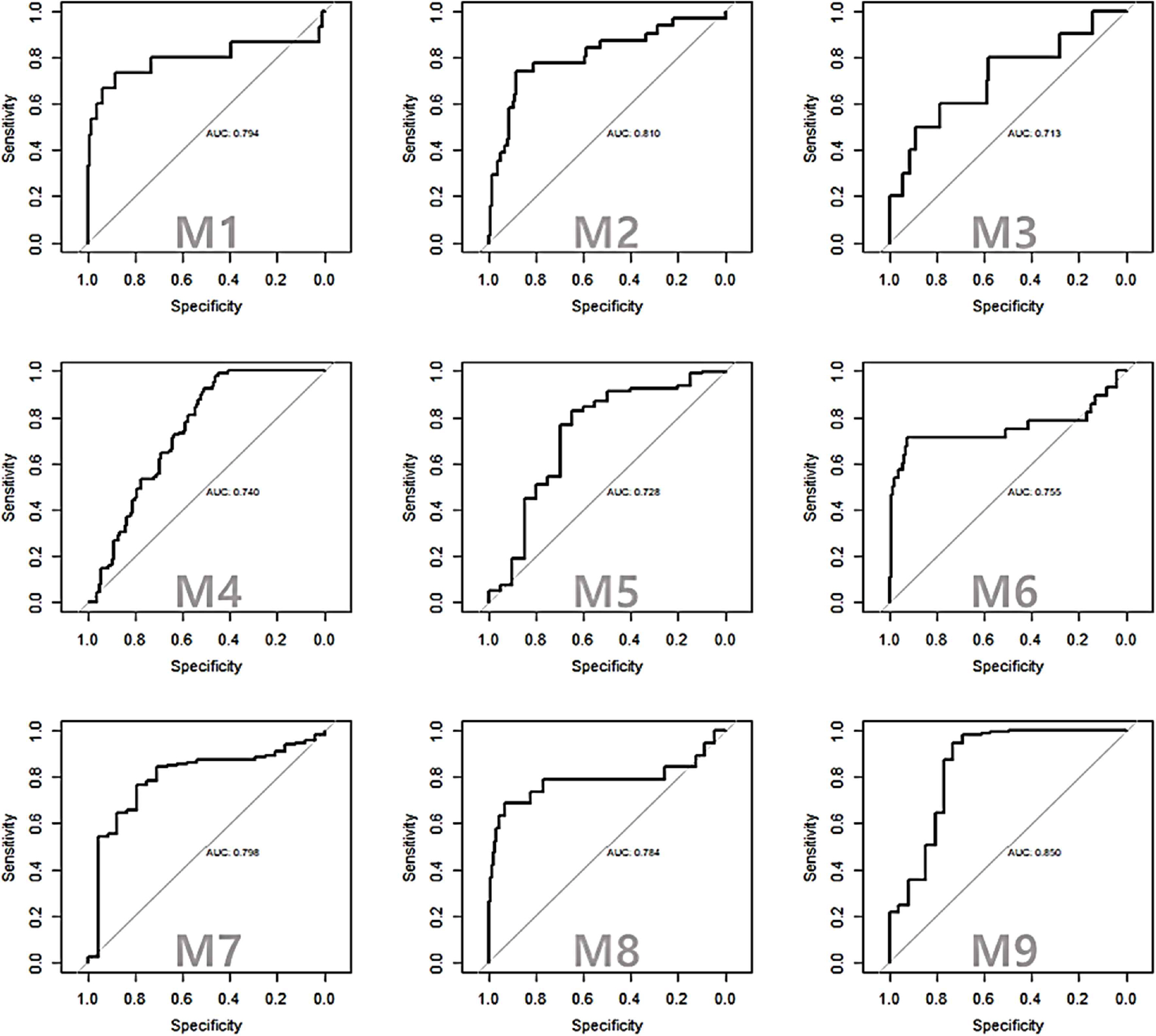

As in Table 6, the first and second MLR models, which are M1 and M2, evaluate the relation between the emergence of unicorn companies and the EE. Since their values denote high R-square values over 0.8. those models have high explanatory power. However, models to examine relationships between the entrepreneurial ecosystem and some dependent variables like the new business registered density (M3) and the employment rate (M4), are not meaningful by having a low coefficient of determination below 0.7. Thus, this paper rejects M3, and M4 and considers the entrepreneurship ecosystem has a low correlation with new business registers, and employment. This can imply entrepreneurial ecosystem contributes to innovation rather than the pure quantity of businesses but quality by leading emergence of the unicorn company. Also, as M2 has a higher R-square value than M1, EE can have more impact on the value of the unicorn value than the unicorn number.

According to significant models, which are M1 and M2 in Table 6, the economic variables such as current account balance (CAB) and foreign direct investment (FDI) are significant relations to the dependent variables. However, contrasting to the FDI, CAB negatively impacts the number of unicorn companies and their valuation. Likewise, in the case of the United States which has various valuable unicorn companies but has a current account deficit, depending on the nation's economic status is an export-lead growing economy or innovation lead economy, the existence and value of a unicorn company can have a negative relationship with a current account (Blanchard, 2017). Financial variables such as lease, utilization, lending flow, and collateral have a significant relation to the number of unicorn companies. Since the start-ups require a considerable amount of seed money and investment for growth, these financial variables would be critical to the businesses. However, as on the table, except for the lease which contributes to the production of the business, most of the significant values such as utilization fee, lending flow, collateral, etc. seem like having negative relation with the unicorn companies. Referring to Cotei and Farhat (2017), as start-ups with high growth opportunities tend to lease the assets, it seems reasonable that the lease has a positive relationship with the unicorn company. Also, as highlighted during the global pandemic era, loan, debt, and other liabilities as financial resources have a negative relationship with startups since they deteriorate the financial stability of the company, increases the reliability of government support, and lead the company into the Zombie company (Binh, Huong, & Loan, 2020). Based on this result, this paper assumes that a business under an inferior environment relies on debt, however, if not, the company does not have to depend on liability and has a stable business operational environment to grow into a unicorn. Though the legitimacy/regulatory factor does not have a significant influence, the time to satisfy the government regulation has a negative relationship with a unicorn. In contrast to the low significant relation with the legitimacy/regulatory factor, the social factor denotes meaningful relations with unicorns. Whether having high-risk acceptance, motivation, business service, process innovation, and overall entrepreneurship index has a positive influence on the value and number of unicorn companies.

However, though the number of enterprises (M5) has low relation with EE, it seems like the entrepreneurial ecosystem has a fair relationship with the involvement of business owners (M6) and employees (M7), expectations for job creation (M8), and entrepreneurship (M9). Compared to employee involvement which highly depends on social variables, such as education, motivation, entrepreneurship, and so on, in the case of business owner's involvement, the financial factor including Small Medium Enterprise (SME) lending flow and financing for entrepreneurs has a crucial impact. Moreover, the growth of venture capital has a positive influence on expectations for job creation. Not only for the social factor. but research and development and foreign direct investment influence optimistic expectations of job creation and stimulate business activity.

M9, which excludes GEI from the social factor but sets it as a dependent, has relations with numerous variables. For instance, ease of doing business, urban rate, human development index, and other variables can be summarized into whether it is comfortable to start a business and have the proper social and economic infrastructure to give confidence to entrepreneurs have a positive relation to entrepreneurship. By verifying less tax and regulation contributes to high GEI, less legitimacy and regulation also have a positive influence on entrepreneurship.

Thus, the significant models indicate that the simple principle that a stable society, less regulation, proper financing resources, fair technological support, and an attractive economy to foreign investors represented through high FDI can enhance the entrepreneurship ecosystem and lead to performance as unicorns, entrepreneurship, and high involvement of employees and employers. Political factor such as government-supporting program can be disputable since it has only a weak positive influence on new business registered density. However, weak relationships among EE, governmental support and regulation also have been studied by Barinova, Zemtsov, and Tsareva (2018) that Russian government and state support indicators are not that significant on EE. Thus, this result supports that a fair EE improves the innovation, perceptional and behavioral aspects of entrepreneurship instead of generating an indifferent quantity of new businesses.

Thus, as in Table 8, the stepwise-MLR model has more improved indicators in adjusted R-square value, F-statistics, standard error, and ρ-value, this paper regards the MLR model derived from the StepAIC method as more reasonable. Though all hypotheses are accepted by having a ρ-value less than a confidence level of 95%, within an R-squared level over 0.7, this paper primarily rejects the hypotheses that EE quality has significant influences on new business registered, employment, and the number of enterprises. This can support the argument that fair EE does not contribute to the quantitative expansion of the business and job but can contribute to people's expectations of job creation, innovative companies, and so on as accepted hypotheses. For more explanatory power, using the more improved R-square standard which is over 0.8 and has adjusted R-squared values over 0.75 at least, this paper finally regards models 1, 2, 7, and 9 are accepted. This implies that the unicorn value and its number have considerable relationships with EE quality and the entrepreneurial activity in the early stage of business also has a significant relationship with EE with entrepreneurship represented as GEI.

Though Davari and Najmabadi’s (2018) MLR model has different independent, and dependent variables, and is limited to survey data collected in Iran only, it has similarities in having finance and infrastructure, which are used as sub-variables of technology in this paper, as significant components of EE. However, compared to this paper, Davari and Najmabadi’s study considers support and policy as important. This result could be caused by different measures of categorizing sub-variables of policy and support or compared to the statistical expenditure utilized for governmental support or policy, the perceived importance can be different. Likewise, since this paper tests various entrepreneurial performances using different independent variables based on the PESTEL using global entrepreneurial data, there would be differences with Davari and Najmabadi’s MLR model, as models on this paper have social, economic, finance, and technology as main components generally.

4.3 Performance Evaluation

Park and Kims’ (2018) study predicts the potential students' outcomes from collected data using an Early Warning System (EWS) and Early Warning Indicator (EWI). However, they indicate that diagnostic measures including EWS and EWI do not have performance evaluation measures considering sensitivity and specificity. For instance, in this study, the model for predicting the postsecondary STEM Degree has been tested by three predictors and the number of STEM courses has the highest predictable accuracy having 0.95. Though the ROC-AUC measure is widely used in the engineering and medical field to evaluate the accuracy of measurements, it is also used in the social science field and it is also applicable to measure the MLR model to predict the performance-driven from EE components.

Thus, to evaluate the performance of the MLR model, this paper constructs the confusion matrix to contain the AUC value and ROC curve as Figure 6. Therefore, it has a similar result to MLR’s R-squared value since the inferior models like M3 to M5 have comparative low AUCs of 0.713, 0.740, and 0.728 though these are interpreted as acceptable. Instead, the superior model with high explanatory power like M1, M2, and M9, has a high AUC over 0.8 which has good performance. Though models 6, 7, and 8 have acceptable performance over 0.75 and fair R-squared values since their performance does not reach a fair level of 0.8, this paper finally considers models M1, M2, and M9 as reasonable models for EE quality-performance relationship.

5. Conclusion

The Entrepreneurship Ecosystem is a significant issue that determines the further competitiveness of the nations by cultivating profitable businesses with innovative ideas. Therefore, to reveal a competitive company that can grow as a global major company in the future, it is important to ensure the opportunity to start the business and stimulates challenge. Thus, there are numerous political attempts to formulate an entrepreneurial ecosystem by the government. Therefore, to verify which factors are significant to EE, this study conducted an MLR analysis

Based on the analysis, rather than political and regulation from the government, finance, economy, technology, and social factors are included as significant variables forming the entrepreneurial ecosystem. Also, models having the number of unicorn companies (M1), their economic value (M2), perceived entrepreneurial activity (M7), and global entrepreneurship index (M9) as performance targets indicate to be more reasonable by having 0.895, 0.898, 0.806, and 0.823 r-squared value each which are over 0.8 under 95% confidence level. However, referring to the performance evaluation of each MLR model in addition to their p-value and r-squared value, models 1, 2, and 9, which denote the emergence and performance of innovative companies and entrepreneurship of the country, have better performance in prediction by having 0.79, 0.81, and 0.85 AUC.

Through this analysis results, this study has practical implications that the EE should focus on encouraging entrepreneurial culture and social infrastructure, cultivating technology, and managing a favorable and stable economy rather than expanding regulation, governmental support, and financing which are less significant to the entrepreneurship performance or having a negative relationship with it. Thus, when the policy maker designs the entrepreneurship policy, rather than direct political and economic support to the individual companies, it would be effective to invest in the macro-environment of technology, society, and economy. Furthermore, the financial policy also should not be expanding the liability of the company but should be providing accessibility to financial resources for investment. Furthermore, when setting entrepreneurship policies, the policymaker would expect the emergence of innovative companies, an increase in entrepreneurial activity, and an improvement in entrepreneurship, however, it would not be valid in expanding business and employment.

Since the MLR models denoting EE quality and performance have been developed, this study can be progressed into the application by comparing the EE quality of the nations and their policies. However, this study has limitations in using the secondary data collected from various research institutes, and since there are various frameworks for defining EE beyond the PESTEL, this study can be improved by collecting more relevant data and testing various models such as Isenberg's model. Also, since GEI can be used as a parameter, the multivariate regression model, such as the structural equation model (SEM), can also be developed. Also, though the concept of the ESG has been rising recently, this paper replaces the environmental factor of PESTEL with Finance separated from the Economy based on the literature review which does not consider the environment as a major component of entrepreneurship. However, ESG is considered a significant factor that allows sustainable business operation and intensifies the brand, by exploring environmental data, further studies to identify whether an environmental factor has a relationship with EE can be conducted.

To stimulate the business, the general business environment is also important, however, the entrepreneurship environment has been highlighted since it accelerates innovativeness, and commercialization of innovative ideas which vitalize the development. Based on the study, the quality of the EE can have a cohesive relationship with innovativeness represented as Unicorn company, further study to measure innovativeness in multiple aspects and factors influencing EE should be studied intensively.